Quick Answer: The most effective personal finance tips for 2026 combine AI-powered budgeting, early investing, and disciplined debt elimination. Start with a realistic budget, build a 3-6 month emergency fund, then invest consistently – even small amounts. These three steps alone put you ahead of 80% of people your age.

Most people do not fail at managing their money because they are not smart. They fail because nobody ever taught them how to do it. If you are reading this and you want to take control of your finance in 2026 you are in the right place. This could be because you are 22 years old and you just started your job or you are 35 years old and you are finally ready to get serious about your personal finance.

These personal finance tips, for 2026 are not ideas that people were talking about a long time ago. They are new. They are based on what is happening in the world today. Today we have a lot of inflation. It is hard to deal with. We also have tools that use artificial intelligence and these tools did not exist three years ago.. Now it is easier for people to invest their money even if they do not know much about it.

Lets get into it.

1. Build a 2026-Ready Budget That Actually Works

Why Most Budgets Fail (And How to Fix)

There’s a reason most budgets do not work. They are based on what you want to spend not what you really spend. You make a plan that looks great on paper. When real bills show up the whole thing falls apart.

The solution is easy. It is not fun. Get out your bank statements and credit card statements from the three months right now. Do not guess. Look at the numbers. The money you spend on coffee the things you pay for every month that you forgot about the things you buy that you only meant to buy one time but you end up buying every month. Most people find out they are spending twenty to thirty five percent more than they thought they were on things they do not really need.

When you see how you really spend your money making a budget is not about what you want to do it is about what you’re actually doing. Budgeting stops being about what you hope for and starts being, about what you spend.

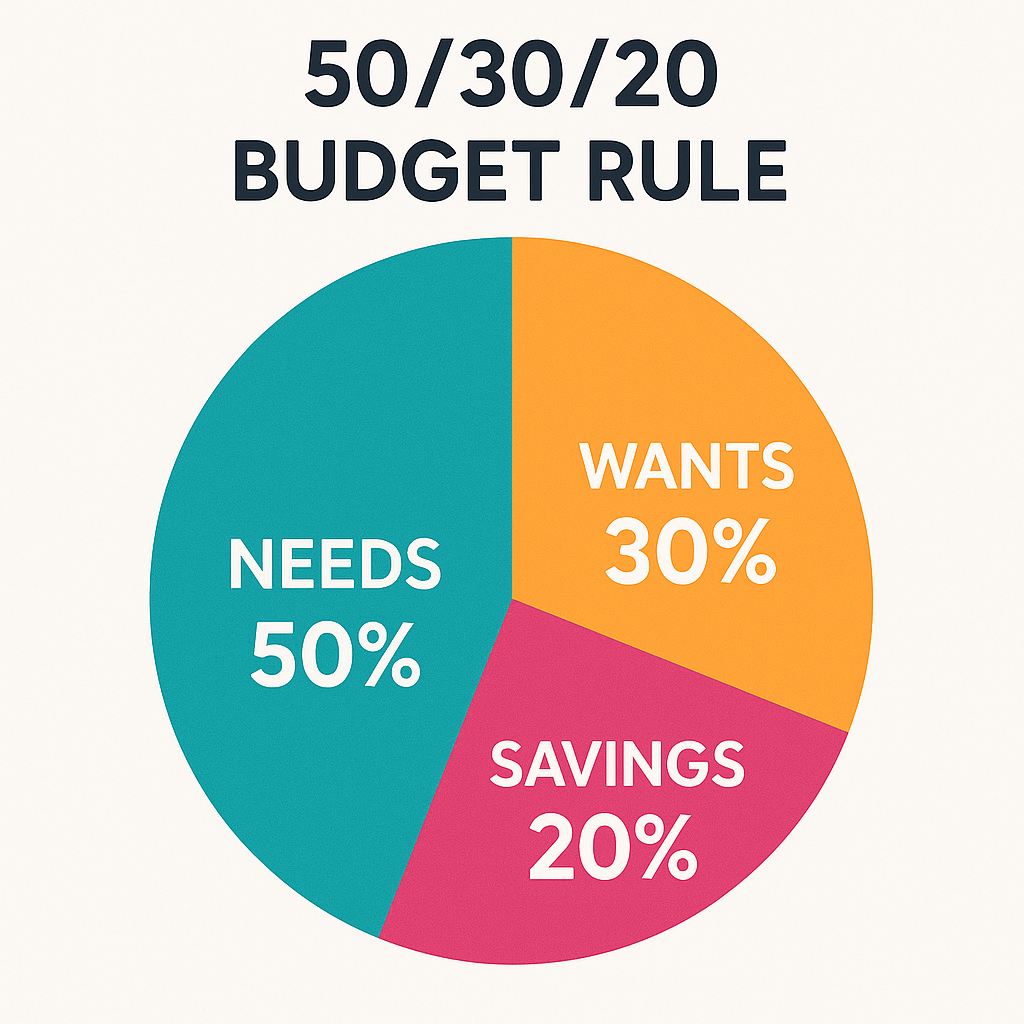

The 50/30/20 Rule vs. Zero-Based Budgeting — Which Is Better in 2026?

Both frameworks work. They’re just built for different people.

| Method | Best For | Core Idea | Effort Level |

| 50/30/20 Rule | Beginners, variable incomes | 50% needs, 30% wants, 20% savings | Low |

| Zero-Based Budgeting | High earners, detail-oriented people | Every $ gets a job; income minus expenses = 0 | High |

| Pay Yourself First | Anyone building long-term wealth | Save first, spend what’s left | Medium |

The 50/30/20 rule gives you breathing room and flexibility, which matters if you’re just starting out. Zero-based budgeting, on the other hand, is almost aggressively precise — you account for every single dollar before the month begins. Neither method matters if you don’t track.

Top AI-Powered Budgeting Tools to Use in 2026

Here’s where 2026 genuinely changes the game. Tools like YNAB (You Need a Budget), Copilot Money, and Monarch Money now use AI to categorize expenses automatically, flag unusual spending, and even predict whether you’ll hit your savings targets based on current behavior. Copilot in particular has gotten remarkably good at identifying subscriptions you might have forgotten.

Start with one app. Pick it. Use it for 30 days before judging it.

How to start today: Download one budgeting app and connect your primary checking account. Don’t customize anything yet — just let it run for two weeks and show you the data.

2. Set Financial Goals That Are Specific, Measurable, and Time-Bound

Short-Term vs. Long-Term Financial Goals — Examples for 2026

Setting goals is not really helpful if you do not have a clear plan. Saying you want to save money is not a real goal. A real goal is something like saving four thousand eight hundred dollars by December 31 2026 by moving four hundred dollars from your account on the day of every month.

You can make goals for this year. These are called short term goals. For example you can try to save one thousand dollars for emergencies pay off one of your credit cards or spend one hundred and fifty dollars less on food every month.

You can also make goals, for the few years. These are called long term goals. For example you can try to have a worth of fifty thousand dollars put as much money as possible in your retirement account every year or buy your first investment property.

How to Use the SMART Goal Framework for Personal Finance

The SMART goals are Specific, Measurable, Achievable, Relevant and Time-bound. This means that when you are tracking your goals you should see actual numbers, not just some idea of what you want to do.

A twenty-five- 25-year-old utilizing the SMART framework might be able to articulate the goal as follows: ‘I will put $200 a month into a low-cost index fund for a year and have $2,400 in the fund by December 2026.’ As mentioned before, SMART has a time- related limitation, an amount associated with the limitation, and something you must do.This goal has a deadline, an amount of money and something you need to do. The SMART goals are really, about being Specific, Measurable, Achievable, Relevant and Time-bound so you can reach your goals.

What Financial Milestones Should You Hit by Age 25, 30, and 35?

These are not rules. They are things to think about. When you are 25 years old you should try to have no debt that costs a lot of money to pay back and a little money saved in case something bad happens. When you are 30 years old you should try to have one years worth of salary saved up in all of your accounts. When you are 35 years old retirement savings should be two times what you make in a year which is what Fidelitys research says.

If you do not meet this goal do not get too upset. The main thing is to keep making progress not to be perfect, with your retirement savings and emergency fund and debt.

3. Build an Emergency Fund Before You Invest a Single Dollar

How Much Should Your Emergency Fund Be in 2026?

A good idea for money is to save about 3 to 6 months of the money you need to live. This way you can handle things that happen like losing your job or having to pay for something you did not expect without getting worried about money. Since the economy in 2026 is still not totally sure because of the problems that happened around the world in the last few years I think it is better to save for 6 months if you have a job that is not very stable or if you work for yourself.

Keep this in mind: don’t stress about saving just the right amount. Having $500 set aside beats nothing at all, since it’ll prevent you from relying on credit cards when your car needs repairs. So go ahead and begin saving now, saving more quickly possible.

Where to Keep Your Emergency Fund for Maximum Growth

Your emergency money should be easy to get to and not mixed with the accounts you use for spending. Those special savings accounts that pay interest you know the ones they call High-yield savings accounts are still pretty good in 2026. They pay interest than regular banks. Some of them pay around 4 to 5 percent interest, per year depending on when you are looking at this.

Do not put your emergency money in the stock market. That is just not an idea. The whole point of having emergency money set aside is so you have something to fall back on not so you can try to make more money.

A simple step-by-step plan to build your emergency fund from scratch helps you stay financially prepared, even if you’re starting with zero savings.

Set up a savings account at a different bank from where you keep your checking account.

Then set up transfers of a fixed amount. Like fifty dollars a week.

Do this transfer the day after you get paid.

Whenever you get money like a tax refund, bonus or birthday cash use it to add to your savings.

This way you do not have to think about saving; the money is moved automatically.

That is why automatic transfers work better, than trying to save.

4. Eliminate High-Interest Debt Using a Proven Strategy

Debt Avalanche vs. Debt Snowball — Which Method Wins in 2026?

The debt avalanche method is about paying off the debt that has the interest rate first. This helps you pay interest over time and become debt free faster.

The truth is that the best method is the one you will really use. Studies have shown that people who use the method are more likely to stay debt free for a long time. This is because feeling motivated is just as important as the numbers.

Let us say you have a credit card with $500 on it and another credit card with $12,000 on it that charges 22 percent interest. If you pay off the $500 credit card first you will pay a bit more interest.. The feeling you get from paying off that first debt is really powerful. The debt avalanche method and the snowball method are both, about paying off debt. The snowball method can give you a sense of accomplishment that helps you keep going. Paying off the debt avalanche method debts can take a time but paying off the snowball method debts can give you a feeling of winning that helps you stay on track.

How to Negotiate Lower Interest Rates on Credit Cards

Call the company that gave you your card and ask them. It really does work a lot of the time. Tell them about all the times you paid your card bill on time and let them know that you got offers, from other cards. If the first person you talk to says no ask to talk to someone who can help you like a retention specialist. If you owe $5,000 on your card and they lower your interest rate by 5% you will save $250 every year.

The Hidden Cost of Minimum Payments — A Real-World Example

So you have a credit card balance of $3,000 with a high interest rate of 20%. If you only pay the minimum amount, which’s around $60 every month it will take you more, than seven years to pay off the credit card balance. You will also have to pay $2,400 in interest. That is a lot of money. The credit card balance of $3,000 will almost double because of the interest. Managing your debt is very important. This is a good example of why you should do it. Managing your credit card balance and debt is crucial.

5. Start Investing Early — Even With a Small Amount

Why Time in the Market Beats Timing the Market

People often believe that investing is about buying at the right time but the truth is that leaving your money invested for a long time usually gives you better results.

Compound interest is something that you hear about a lot. When you see the actual numbers it is really powerful. For example if someone puts $200 into an investment every month starting at the age of 22 and they get a return of 8 percent each year they can turn it into about $702,000 by the time they are 62 years old.

If they start investing the $200 every month at the age of 32 they will only have around $298,000 when they are 62 years old.

They are investing the amount of money every month and getting the same return the only difference is the time they started investing and that difference can cost them around $400,000.

Best Investment Vehicles for Beginners in 2026

Lots of people believe that investing successfully is about starting with the accounts. You should begin with tax- accounts before you do anything else. If the company you work for offers a 401(k) match you should put in money to get the full match. It is basically like getting a 50 to 100 percent return on that part of your money right away.

After you do that a Roth IRA is a good option for the long term if you make enough money to qualify for one. This is because when you retire you can take out the money without paying any taxes on it.

For investing on a basis index funds that follow the S&P 500 are still a good choice. They might not seem exciting but they have proven to be trustworthy, over a long period of time.

[INTERNAL LINK: beginners guide to Roth IRA investing → how Roth IRA works for investors]

How to Start Investing With $50 or Less

Getting started with investing does not require a lot of money anymore. You can use platforms like Fidelity, Charles Schwab and M1 Finance to invest without needing a lot of money to start.

You can even buy a part of major index funds with just one dollar, which makes it easier for people who are new to investing.

At this point investing is not about how money you start with it is about taking that first step with your investments. You should open an account with Fidelity, Charles Schwab or M1 Finance invest the money you can and keep doing it because investing regularly with these platforms matters more, than the amount of money you start with when you begin investing with Fidelity, Charles Schwab and M1 Finance.

6. Maximize Tax Advantages Before You Lose Them

What Tax-Advantaged Accounts Should You Use in 2026?

There are three accounts that’re really important. Your 401(k) is one of them. It is for saving money before you pay taxes for when you retire. The most you can put in your 401(k) in 2026 is $23,500 if you are under 50 years old.

Another important account is a Roth IRA which helps your money grow without paying taxes. In 2026 you can put up to $7,000 in a Roth IRA.

Then there is a Health Savings Account, which’s also very important if you have a health plan that requires you to pay a lot of money before it starts to cover your expenses. A Health Savings Account is special because it has three advantages when it comes to taxes. When you put money into a Health Savings Account it is before you pay taxes. The money in a Health Savings Account also grows without you paying taxes.. When you take money out of a Health Savings Account to pay for medical bills you do not have to pay taxes on that money either. A 401(k) and a Roth IRA and a Health Savings Account are all important, for reasons.

Above-the-Line Deductions Most People Miss

Student loan interest, self-employment health insurance premiums, and contributions to a traditional IRA are all above-the-line deductions — meaning you can claim them even without itemizing. Freelancers and side hustlers especially leave money on the table here every year.

Should You Consult a Tax Professional or Use Software in 2026?

Tax software (TurboTax, H&R Block, FreeTaxUSA) handles straightforward situations well. But if you have freelance income, investments, a rental property, or significant life changes — marriage, a new child, a business — a Certified Financial Planner (CFP) or CPA pays for themselves quickly. Use the IRS’s BrokerCheck tool to verify any financial advisor’s credentials before handing over your financial life.

7. Grow Your Income With Passive and Side Income Streams

What Is Passive Income — And Is It Really “Passive”?

Let us be direct about something that social media gets completely wrong. Almost no passive income is passive income, in the beginning. Dividend investing requires capital that you have to accumulate. Rental properties require management and maintenance and often debt. A digital course requires dozens or hundreds of hours to build. The passive income part comes after upfront work or capital.

That does not make these passive income ideas bad. It makes these passive income ideas realistic.

Top 5 Realistic Passive Income Ideas for 2026

- Dividend-paying index funds or REITs — invest regularly, reinvest dividends, and let compounding do the work over years.

- High-yield savings accounts and CDs — not glamorous, but actually passive with zero effort.

- Peer-to-peer lending platforms — carries more risk, but some investors see 6–9% returns.

- Selling digital products (templates, presets, ebooks) — high upfront effort, genuine passive revenue afterward.

- Licensing photography or writing — if you already create content, monetize it through stock platforms.

How to Start a Side Hustle That Complements Your 9-to-5

People usually make a mistake when they look for a side job that pays the money. They should look for a side job that they can keep doing for a time. The best side job is one that uses something you’re already good at. It should make you feel happy and not tired.

You can write for people give advice in the field you work in teach someone something or make computer programs. These things help you get better at your job and also make you some money. Your side job should be something, like freelance writing or consulting in your field or tutoring or building software tools.

8. Protect Your Wealth With the Right Insurance Coverage

Why Insurance Is a Wealth-Building Tool (Not Just a Safety Net)

One uninsured medical emergency, car accident, or house fire can eliminate years of financial progress in a week. Insurance isn’t a cost — it’s the floor beneath your wealth-building plan.

Essential Insurance Policies Every Young Professional Needs in 2026

Young professionals might still skip over insurance despite growing financial responsibilities; having some coverage becomes indispensable with age.

Some insurance policies should really be part of your setup. Health is certainly one, it’s something you just can’t live without. Renter or homeowner policy needs consideration, as well as protection for vehicles if owned. Those dependent on income could consider term life coverage. If someone relies on the money you make you need term life insurance. A lot of people do not get long-term disability insurance but they really should get it. The fact that you can earn money is the important thing when you are, in your 20s and 30s. Long-term disability insurance is something that young professionals often skip. They almost always need it. Your ability to earn an income is your valuable asset and you need to protect it with long-term disability insurance.

How to Review and Optimize Your Insurance Without Overpaying

Review all insurance policies at least annually. Compare quotes from competing providers every two to three years — loyalty rarely pays in this industry. Look for policy bundling discounts (home and auto together typically saves 10–25%), and always update your beneficiary designation forms after major life events like marriage, divorce, or having children.

9. Improve Your Credit Score Strategically

What Actually Affects Your Credit Score in 2026?

Your credit score breaks down roughly as follows: payment history (35%), amounts owed / credit utilization (30%), length of credit history (15%), new credit (10%), and credit mix (10%). Most of the weight sits in just two factors — pay on time and keep utilization below 30%.

How to Raise Your Credit Score by 50–100 Points

Pay all your bills on time. Even if you can only pay a little it helps. On-time payments prevent charges and protect your credit score.

To get the score keep credit usage below 10%.

If you find mistakes on your credit report tell Equifax, Experian or TransUnion directly. They will help you fix it for free.

Don’t close accounts. They help your credit score because they show a credit history.

Services that monitor your credit alert you when something changes. This also helps catch fraud

* Pay bills on time it is good for credit score.

* Keep credit usage low below 10% is ideal.

How a Good Credit Score Translates Into Real Wealth

A credit score of 760 is really different from a credit score of 620 when you are talking about a mortgage of $300,000.

The monthly payments can be $200 to $400 more with a 620 credit score.

This means you will pay $72,000 to $144,000 in interest over thirty years.

That is a lot of money.

The reason for this difference is your credit score.

You can improve your credit score with two years of being careful with money.

A 760 credit score can save you a lot of money on a $300,000 mortgage.

So it is worth trying to improve your credit score.

A good credit score like 760 can make a difference, in how much you pay for a $300,000 mortgage.

10. Build a Long-Term Wealth Mindset — The Habit Layer

The Behavioral Finance Traps That Keep People Broke

Most personal finance guides do not talk about something. The math of building wealth is really simple.. The psychology of building wealth is where people have problems. When your income goes up you might start spending money this is called lifestyle inflation. It can hurt your wealth more, than making investment decisions.

You get used to things fast so the joy of having a bigger apartment or a newer car does not last long.. You have to pay for these things for a long time. Building wealth is hard because of the way people think. Some people hold on to investments that are losing money because they want to get back what they lost. At the time they sell investments that are making money too early. This is the opposite of what you should do to build wealth. Building wealth with finance guides and the psychology of wealth-building is not easy. Lifestyle inflation and the psychology of wealth-building are problems.

Daily, Weekly, and Monthly Financial Habits of Wealth Builders

Daily: Take a minute to look at your account balances. Not all the time. A quick glance.

Weekly: Check your budget app to see how you spent your money.

Monthly: See how your investments are doing check if you are on track to meet your goals and make any changes you need to.

Quarterly: Look at your investments to make sure they are still right for you check if your insurance still makes sense and see what your credit score is.

Building wealth over time is more, about doing these things than making one big choice.

How to Stay Consistent With Your Financial Plan When Life Gets Hard

Life will get in the way of your plans. You might lose your job get a medical bill or have a family problem. The idea is not to stick to your plan but to have things set up so they keep going even when you are busy with other things. For example if you set up transfers to your savings account the money will keep going in even when you are not thinking about it. Having some extra money saved up for emergencies means that a bad month will not be a disaster.

You should talk to an advisor who is required by law to do what is best for you not just try to make money from you when big things happen in your life. This could be when you get a lot of money from someone start your business or get close to retiring. Getting advice, from a professional at the right time is worth paying for.

Frequently Asked Questions

What are the most important personal finance tips for beginners in 2026?

First you need to do three things. Create a budget that is based on what you spend, not what you think you spend. Then you need to save one thousand dollars in an emergency fund before you do anything else. You also need to get rid of any debt that has interest as quickly as you can.

Once you have taken care of these three things you can start investing. You do not need to invest a lot of money even small amounts are okay. Just make sure you are putting your money in an account that helps you save on taxes. The order that you do these things is important. If you are investing money while you still owe a lot of money on your credit card with an interest rate, like twenty two percent it does not make sense. Investing and having high-interest debt at the time is like taking two steps forward and one step back. You should focus on getting rid of the high-interest debt like the debt, on your credit card and then start investing.

How much money should I secure each month?

The 20 percent benchmark from the 50/30/20 rule is a place to start.. The situation you are in is important. If you have debt with interest you should try to pay more, than 20 percent of your money towards getting rid of that debt first. If you do not have any debt you might want to think about saving 25 to 30 percent of your money if you can afford to do that now. The truth is that saving money is almost always a good thing but it is better to save some money than to save no money at all.

What is the best investment strategy for a 25-year-old in 2026?

First you should try to get the most out of your employers 401(k) match. This is basically money.

After that you can put money into a Roth IRA up to the limit they let you.

When you invest look for funds that do not cost a lot and have a bit of everything in them.

Total market funds or S&P 500 funds are choices if they charge less than 0.10%.

At this point do not worry much about picking individual stocks.

Investing in stocks requires a lot of experience and research and you have to understand the risks.

It is better to stick with investment options that’re safer and more stable.

You can do this until you have an understanding of how investing works.

What is important at your age like 25 is to be consistent and give your mone

How do I start building wealth with a low income?

Building wealth when you do not have a lot of money is really tough. It is not something that cannot be done. You have to focus a lot on two things: reducing the amount of money you spend on big things like where you live and how you get around and finding ways to make more money over time by learning new skills. Even putting twenty five dollars per month into a Roth IRA is a start because it helps you get into the habit of saving and it also helps your money grow. Every time you get a raise or some extra money you should use it to make a difference, between how much money you make and how much money you spend. Becoming financially independent takes a time and the only thing that really matters is that you start doing something about it. Building wealth and financial independence is what you need to focus on.

Start with one section. Not ten. Pick the area where you know you’re weakest — budget, debt, emergency fund — and spend 30 focused days there. Real financial growth is built one disciplined decision at a time.

SEO & Technical Elements

SEO TITLE (52 chars): 10 Personal Finance Tips 2026 to Build Real Wealth

META DESCRIPTION (158 chars): Discover 10 proven personal finance tips for 2026. Learn how to budget smarter, eliminate debt, start investing, and build lasting wealth — even on a tight income.

URL SLUG: personal-finance-tips-2026

FOCUS KEYWORD DENSITY CHECK: “personal finance tips 2026” appeared 4 times (first 100 words, H1, intro, FAQ)

SUGGESTED IMAGE ALT TEXT 1: Personal finance tips 2026 — budget planner and savings tracker on desk

SUGGESTED IMAGE ALT TEXT 2: How to build wealth in 2026 — young professional reviewing investment portfolio on laptop

SCHEMA TYPE RECOMMENDED: Article + FAQ (dual schema — Article for the main body, FAQPage for the FAQ section at bottom